While oil garnered the headlines, interest rate moves remain the key driver for the markets, as they weigh the impact of inflation and growth on the economy, as well as the path for Fed policy. Importantly, with Kevin Warsh taking over as the new Fed chairman, the market is closely watching his policy preferences. But like most Fed leaders, reacting to the economy will most likely dictate Chairman Warsh’s policy moves.

Chart 1

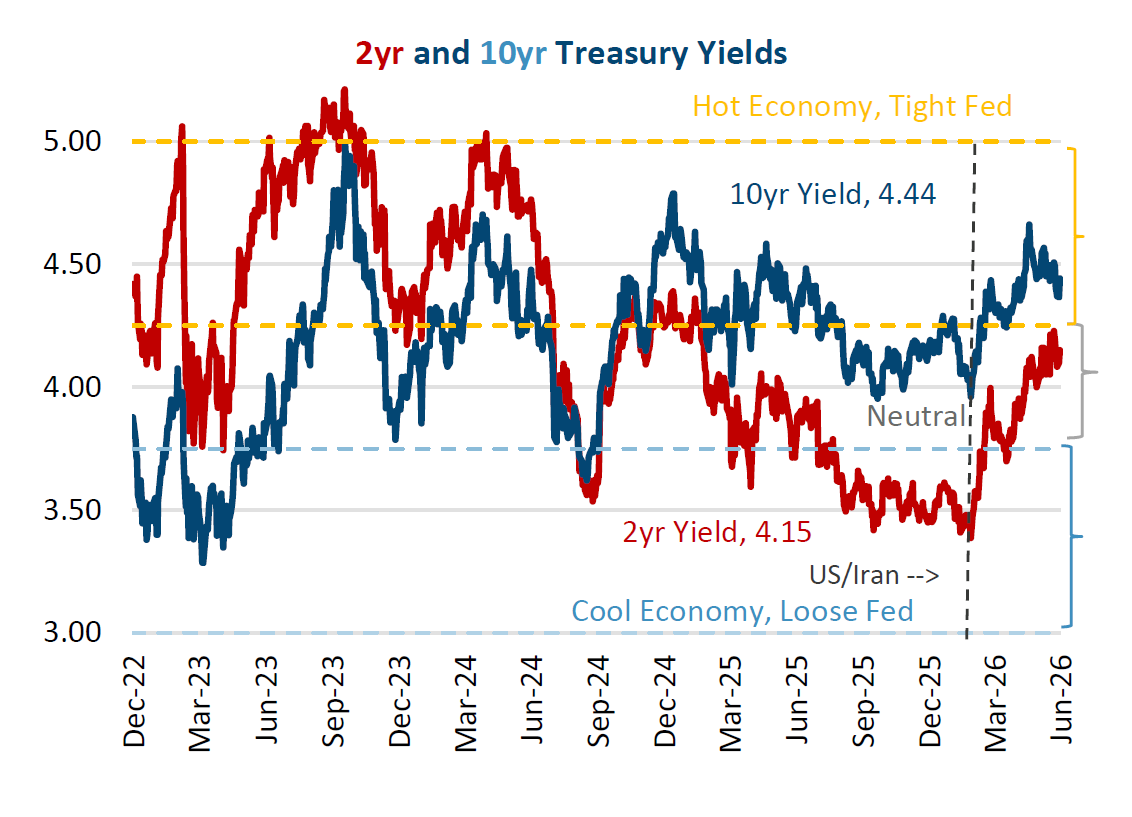

Comparing economic and Federal Reserve expectations to levels currently implied by interest rates remains the best way to frame these types of debates.

Our “market expectations” model compares current market interest rates relative to the embedded Fed and economic expectations. Assuming 2% inflation and 2% trend growth, we get a 4% neutral interest rate, bracketed by a 50 bps 3.75% to 4.25% neutral range. The chart shows the 2yr (Fed policy) and 10yr (economy), as well as orange “Hot Economy, Tight Fed” and a blue “Cool Economy, Loose Fed” ranges.

At the start of the year, the economic data and the expectation of a new chairman had the market pricing a “neutral” economy with the 10yr at 4.17% on 12/31/25 and “cool” Fed with the 2yr at 3.48%, then drifting lower through February. Then expectations shifted with the U.S. military action in Iran. While the 10yr has risen 49 bps from a February low of 3.95% to 4.44% by the end of Q2, the move in the 2yr has been larger, rising from 3.45% to 4.15%, or 70 bps, in the same period.

With the 2yr sensitive to Fed policy, a 70 bps move is essentially the market adding three 25 bps rate hikes (totaling 75 bps) to its Fed expectations. With the Fed target rate currently at 3.50%, that is the market going from expecting one rate cut to two rate hikes. While oil prices are seen as transitory, their inflation impact was still enough to push off the chances for the Fed to make more rate cuts. But the big spike (which pushed the 2yr above 4% and the 10yr over 4.5%) came on May 8, with strong payrolls on the unemployment report. The combination of rising inflation pressures and a solid labor market took the prospect of Warsh making additional rate cuts off the table, as far as markets were concerned.

The good news is that while rising interest rates were a headwind for Q2 and YTD bond returns, it presents better yields for investors entering the second half of 2026. Additionally, the more balanced market expectation means a mere moderation in the outlook for the Fed and/or the economy could allow duration to shift to a benefit for bond returns.

The original expectation was that Chairman Warsh would resume the Fed’s recent rate cutting campaign. However, Chairman Warsh’s Hands Are Tied by macroeconomic developments of inflation pressure and a solid labor market. The positive is that with the bond market now pricing one or two Fed rate hikes in 2026, if the Fed can merely hold rates steady, that could be a tailwind to both bond and stock returns for the balance of the year.