Markets rallied through most of Q2, despite the ongoing geopolitical headlines of disrupted oil through the Strait of Hormuz and rising interest rates amidst shifting Fed policy views.

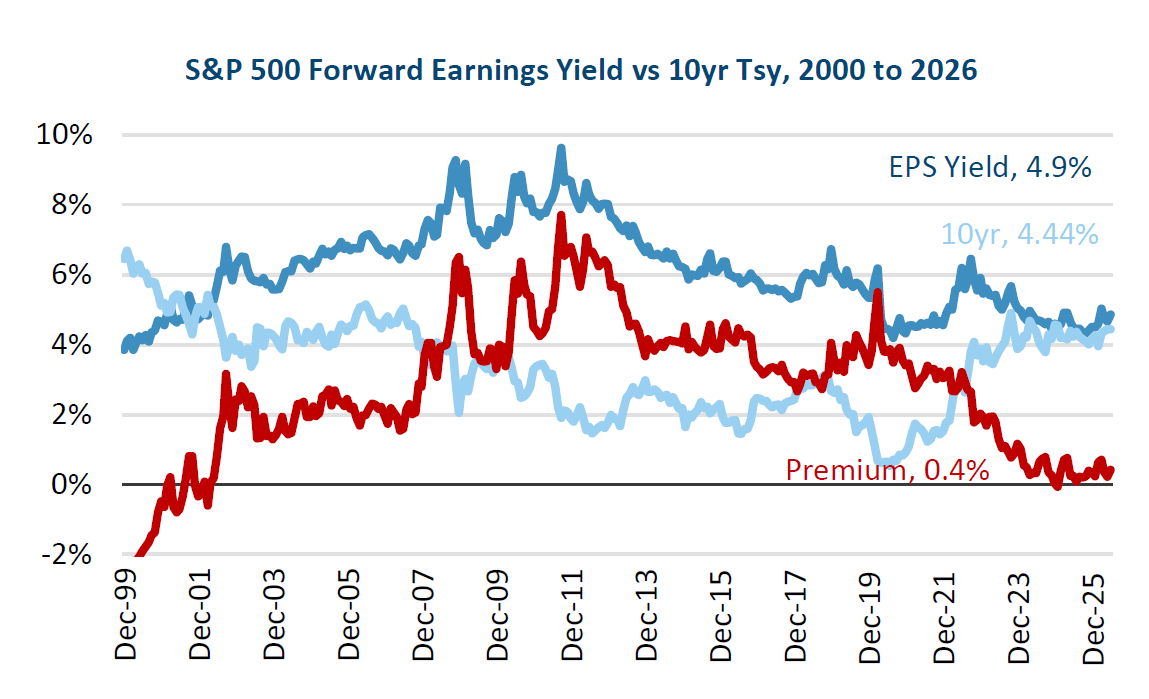

Chart 1

This can help be explained by the relationship in the chart above showing the earnings yield on the S&P 500, the yield on the 10yr Treasury, and the difference between the two, known as the Equity Premium. A higher Equity Premium means stock investors are getting more compensation relative to bonds.

From 2002 to 2007, prior to the Fed’s QE interventions, a 1-3% Equity Premium was common. Recently, the Equity Premium has been near the low end of this range, making the stock market sensitive to interest rate moves. In particular, with the Earnings Yield in the 4.50% to 5.00% range, stocks get sensitive when interest rates approach that 4.50% level due to pressure on the Premium.

Although the 10yr rose 12 bps to 4.44% during Q2’26 and the S&P 500 rose 15%, the earnings yield held steady at 4.9%, so the Earnings Premium was still 0.4%, the same level it started the year. In other words, strong earnings reported during Q2 have helped to support the stock market.

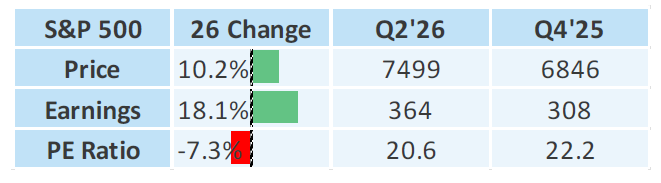

Chart 2

This is evident in the table above. As of the end of 2025, the S&P 500 PE was 22. While the S&P 500 has risen 10% year to date, its profits have risen by 18%, so even as the price is higher, the PE multiple has declined to 21. When the PE ratio is down, that means the earnings yield is up, and this has allowed the Equity Premium to hold up despite both higher interest rates and a rising stock market.

Drilling down within the S&P 500, the Technology sector’s 19% year-to-date return is among the leaders (along with Industrials and Energy) and, more importantly, its 37% forward profit growth only lags the oil-boosted Energy sector. Consequently, the S&P 500’s largest, and top performing, sector has seen its PE ratio fall by 13% (from 27 to 23), which has been key to the overall market’s falling valuation.

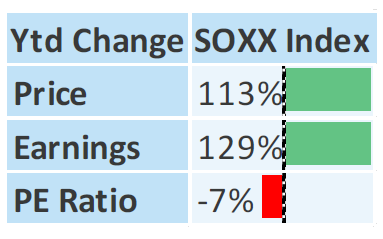

Chart 3

Within the Technology sector, the big story in 2026 and, especially Q2, has been the performance of semiconductor stocks. Applying this same analysis to the Philadelphia Semiconductor Index (SOXX) shows a remarkable story.

Chart 4

For the first half of the year, the SOXX has risen 113%. Yet its forward profit estimates have grown faster, by 129%, and thus the PE ratio has actually declined by 7%, from 32 to 30. This is the result of surging AI demand for semiconductors outstripping supply and causing a significant increase in both revenues and margins.

This underscores the importance of Technology sector profit growth, and its underlying AI driven demand for semiconductors, to the market’s strong performance. During this period of geopolitical uncertainty and questions over Federal Reserve policy, the importance of AI spending has remained the primary story, which is driving profit growth in the stock market.

It is a reminder that the main driver of equity market returns is profit growth. That is why Flush Corporate Profits Beat a Disrupted Strait. And it is a reminder that going forward, the market will remain more sensitive to AI spending trends than geopolitical developments.