Many women find themselves working with a financial advisor through a spouse, a life event, or a decision to seek additional guidance. But the real question isn’t how you got there—it’s how you want the relationship to work. The structure is yours to define and refine as your needs evolve.

How to know when it’s working

The most effective advisor relationships are built around your preferences, how you process information, weigh decisions, and choose to stay involved over time. You may notice it working well when:

- Decisions feel aligned with your priorities and values

- You feel organized, informed, and engaged in the process

- You understand not just what is recommended, but why it matters

- Conversations feel collaborative rather than directive

- You leave meetings with greater clarity and confidence

At its best, the relationship reinforces your role as the decision maker, rather than replacing it.

Start with yourself

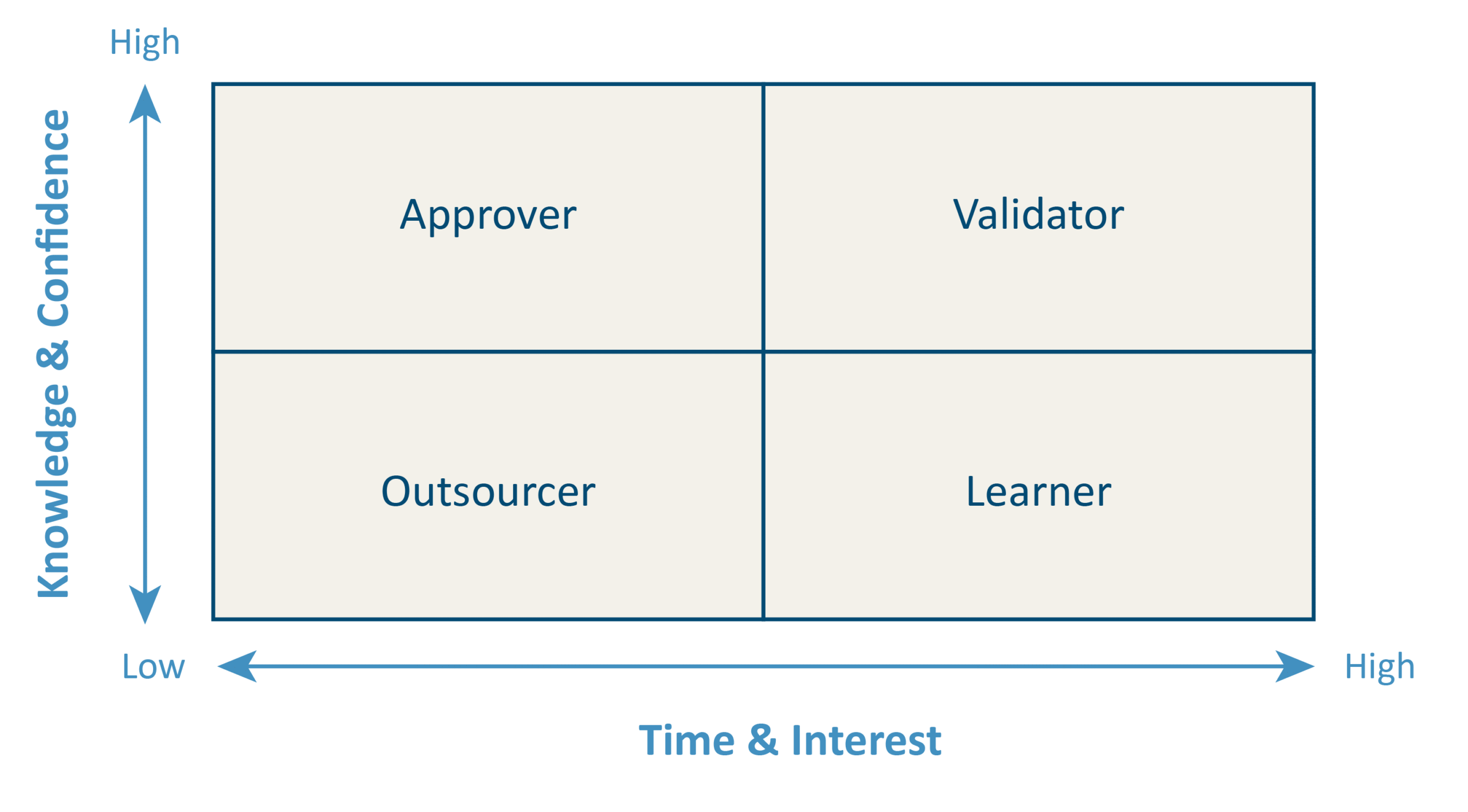

Women engage advisors in different ways, shaped by their experience, preferences, and expectations. A helpful place to start is by reflecting on two dimensions:

- Knowledge and confidence: How comfortable do you feel with financial concepts and decisions? Do you understand how your finances are structured and why? Do you stay informed on market happenings and tax law changes? Do you prefer to make decisions independently, collaboratively, or to rely on others?

- Time and interest: How much time and energy do you want to devote to your financial life? Do you find financial organization and planning engaging, or prefer to move through it efficiently? Do you have the time and capacity to stay organized and follow through on key tasks?

Depending on your answers, you may find yourself aligning with one of four approaches:

APPROVER: You feel knowledgeable and up to date on financial topics but have limited time or energy to stay close to the details. You prefer to delegate the day-to-day execution and rely on a spouse, partner, or advisor to manage the details and keep things moving.

When it’s working: You review and approve important decisions at critical milestones and feel confident that the day-to-day is being well managed.

VALIDATOR: You are knowledgeable and confident in financial decision-making and enjoy managing the details of your financial life, but you value an additional perspective to ensure nothing is overlooked. You bring ideas to your advisor to pressure test your thinking and explore trade-offs before taking action.

When it’s working: You feel more informed and confident in your decisions and are willing to refine your approach when new insights from your advisor add clarity.

OUTSOURCER: You prefer to step back from active management of your financial life and rely on a trusted partner to manage both decisions and execution. Rather than building deep financial knowledge yourself, you place confidence in a spouse, partner, or advisor to guide the direction.

When it’s working: You feel a sense of ease and trust, knowing your financial life is being thoughtfully managed, without needing to stay closely involved.

LEARNER: You are motivated to build your knowledge and become more confident in your financial decisions. You look to your advisor as a resource center and guide—someone who can explain concepts clearly, answer questions without judgment, and create space for you to learn.

When it’s working: You feel supported, not intimidated, and your understanding deepens over time.

These roles are fluid—not fixed—and may evolve over time. As you start a new career, launch a new business, or go through a family transition, your preferred approach may shift as well. The most effective advisors will adjust alongside you, but they can only do so if they understand how you want to engage.

A familiar way to think about it

Choosing a financial advisor is a lot like choosing a doctor. You want someone qualified, but also someone who can guide you, connect you to specialists, and adapt to your needs over time.

You need clear explanations you can act on. A good doctor explains a diagnosis and treatment plan in a way you understand. Your advisor should do the same with your financial plan.

Recommendations should translate into action. A doctor doesn’t just suggest medication; they write the prescription and review it at your next visit. Similarly, your advisor helps move decisions forward and checks in to ensure things stay on track.

They help coordinate the bigger picture. Doctors refer you to the right specialists to bring in the expertise needed for your care. A strong advisor connects investments, taxes, and estate planning so decisions work together.

The approach adapts to you. Care plans evolve as your health changes. Your financial plan, and how you work with your advisor, should evolve as your life and priorities shift.

They’re there for both routine and unexpected needs. Just like wellness visits and sick visits, some conversations are planned and proactive, while others happen when something changes. You should feel comfortable reaching out when a major life event arises.

When the relationship may be misaligned

Even long-standing relationships can drift out of alignment, especially as your needs or circumstances evolve. If you leave conversations with your advisor feeling unheard, unclear, or disconnected from the recommendations being made, it may be time to reset the relationship. Just because women have historically been less involved in financial decisions doesn’t mean you should settle for less. You deserve a relationship that includes you, respects you, and works the way you want it to.

This article is part of our Bridge the Gaps program, focused on helping women investors approach wealth with clarity and intention.

Important Disclosures:

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company Wealth Management, LLC (d/b/a Grimes & Company), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Grimes is engaged, or continues to be engaged, to provide investment advisory services. Grimes is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Grimes’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at https://www.grimesco.com/form-crs-adv/. Please Note: Grimes does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Grimes’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Grimes client, please contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian./