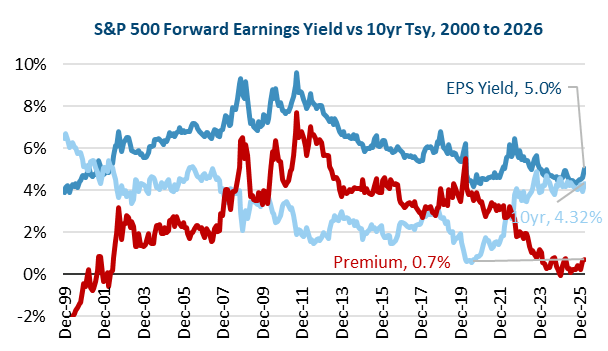

Despite the geopolitical headlines and rising oil prices, stock markets have held up, with the S&P 500 down just 4% in Q1’26 (including 5% since Feb 27), and other indices flat. This can help be explained by the relationship in Chart 1 below, showing the earnings yield on the S&P 500, the yield on the 10yr Treasury, and the difference between the two, known as the Equity Premium. A higher Equity Premium means stock investors are getting more compensation relative to bonds. From 2002 to 2007, prior to the Fed’s QE interventions, a 1-3% Equity Premium was common.

Chart 1

Recently, the Equity Premium has been near the low end of this range, making the stock market sensitive to interest rate moves. In particular, with the Earnings Yield in the 4.50% to 5.00% range, stocks get sensitive when interest rates approach that 4.50% level due to pressure on the Premium.

For example, this relationship helps to explain why the equity markets held up relatively well in Q1, despite the headlines. Although the 10yr rose 15 bps to 4.32% during Q1’26, the earnings yield rose from 4.5% to 5.0%, so the Earnings Premium ROSE to 0.7% from 0.3%. In other words, strong earnings reported during Q1 have helped to support the market.

On the other hand, it was also evident as the Q1 stock market decline intensified in the final two weeks of the quarter, as the 10yr jumped from 4.20% to 4.44%. Oil had already risen by $40 per barrel by this point, and in those weeks went from just $97 to $102. In other words, it was the jump in rates, not oil, that coincided with the stock market decline. From there, the peak 10yr yield at 4.44% was within a day of the stock market bottom in the final week of the quarter, and stocks rose as rates fell to close the period. Of course, oil prices are part of why interest rates are moving, but it is the interest rate changes, not oil prices, that have been driving the stock market.

Interest rates backing away from the 4.5% range is good news, for now. But this framework also shows the risk of an extended disruption to global oil prices. The risk would be that rising inflation continued to push the 10yr yield higher, while the higher cost of energy both squeezed costs and reduced consumer spending, which would pressure earnings. That combination could push the Earnings Premium towards 0, with the only path to equilibrium being a higher Earnings Yield via lower stock prices. At the same time, when an “off ramp” comes into view, the result could be rates moving lower and greater earnings confidence, and thus a positive market response.

It remains the case that in the current environment, the 10yr pushing above 4.5% begins to become a headwind for equity markets, while signs that rates could come back down are a tailwind, as Interest Rates Fuel Stock Market Moves.