While oil captured headlines, interest rate moves have been the primary channel for inflation expectations to enter the financial markets. For Fed policy (and market participants trying to forecast Fed policy), the oil price spike comes at an awkward time, right as the Fed is trying to gauge how much of the fading inflation uptick from last year’s tariff-related factors remains.

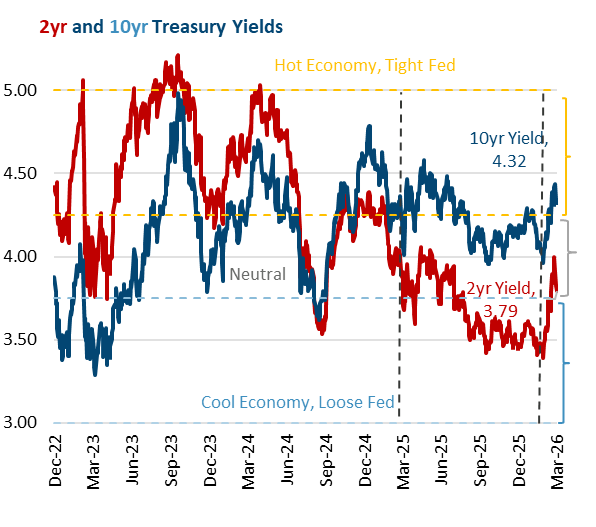

Chart 1

Comparing economic and Federal Reserve expectations to levels currently implied by interest rates remains the best way to frame these types of debates. Our “market expectations” model compares current market interest rates relative to the embedded Fed and economic expectations. Assuming 2% inflation and 2% trend growth, we get a 4% neutral interest rate, bracketed by a 50 bps 3.75% to 4.25% neutral range. Chart 1 above shows the 2yr (Fed policy) and 10yr (economy), as well as orange “Hot Economy, Tight Fed” and a blue “Cool Economy, Loose Fed” ranges. The 10yr has moved 40 bps higher (from 3.95% on 2/27 to as high as 4.44%) in response to rising inflation expectations, while shifting Fed expectations are evident in the 2yr jumping from 3.39% to 3.79%. With the current Fed Funds target of 3.50%, that means the market went from pricing additional rate cuts (3.39% is less than the Fed’s current 3.50% target), to pricing rate increases in the coming two years.

Using the math of the model, the risk is that the economy goes from 3% growth and 2% inflation to 2% growth and 3% inflation. In both cases, long-term rates would be around 5%. But in the latter case, growth is lower and the Fed’s ability to cut interest rates to support the economy is limited. This would be the type of stagflationary risk that can most worry markets.

This situation is similar to the market’s Liberation Day reaction a year ago. In that case, the stock market sell-off was more severe (representing more significant concerns about profit growth), but interest rates started to rise amidst market concerns about tariffs pushing up inflation, instead of falling, as they would in a typical “risk off” reaction when markets price slower growth. The result was stocks and bonds declining at the same time. This time around, the growth concern is not as large, but the 10yr made a very similar jump from below 4% to nearly 4.5%, reaching 4.44% on March 27. That prompted another deadline delay (to April 6) over that weekend, and stock markets bottomed that Monday, then rallied, as rates starting to decline into the end of the quarter.

Just as with tariffs a year ago, rising interest rates help to act as a market signal to policymakers about the risks of a given course of action. Also, just as a year ago, should the disruption dissipate, rates can reverse course and decline, which can be a positive for markets and the economy. This shows that Bonds are Still Vigilant.