401(k) Education and Advice More Important Than Ever

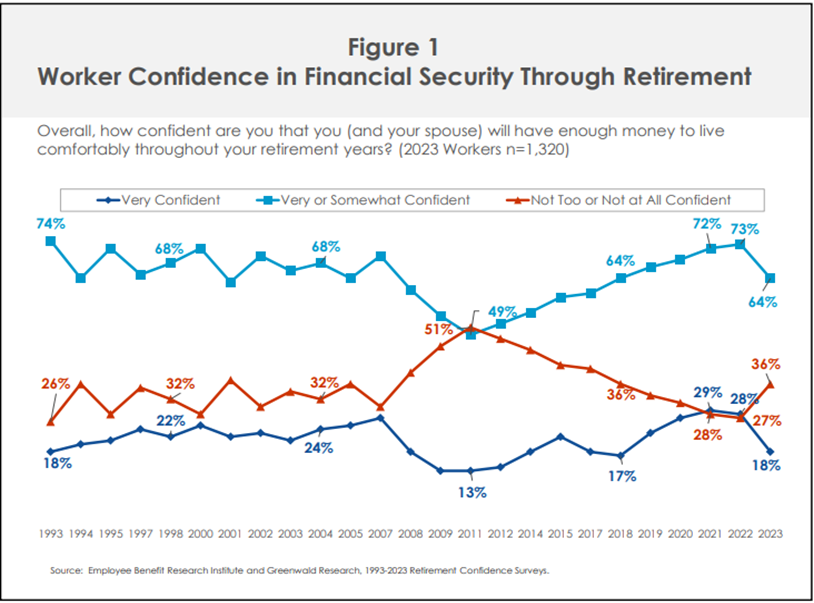

Saving and investing for your retirement can be an intimidating prospect for even the most well-versed investor. An employer can offer a 401(k) plan with a generous match, competitive investment options, and top-notch technology, but without the accompanying financial education, employees can feel intimidated and overwhelmed. The 2023 Retirement Confidence Survey (RCS) found that just 64% of American workers are confident that they will have enough money saved to live comfortably in retirement.(1)

An effective 401(k) employee education program should include enrollment meetings where the different provisions of the plan are discussed along with the investment options. Additionally, employees should be familiarized with basic investment concepts such as time horizon and risk/return. One on one meetings should also be offered so that participants can ask questions specific to their individual accounts. In these individual meetings, asset allocation, fund choices and savings rates should be addressed.

The recent popularity of virtual employee meetings has made employee education even more accessible. Employees can meet with a Registered Investment Advisor (RIA) or listen to a group presentation directly from their desks or homes. Also, online scheduling tools make it even easier to set up one on one meetings.

While the use of technology to reach employees has had a positive impact, a recent study by Charles Schwab found that workers are still more likely to follow financial advice from a human as opposed to computer generated advice. The same study found that workers’ ability to make financial decisions increased with the help of a financial professional. (2)

In addition to benefitting employees’ financial wellness, plan sponsors should also view providing employee education as a best practice as a fiduciary. If you make decisions that impact your company’s retirement plan, then you are most likely a fiduciary as defined by the Employee Retirement Income Security Act of 1974 (ERISA).

Unfortunately, there is no guarantee that offering employee education will ensure an employee’s participation. A regular schedule and a personal touch can certainly help. But as with most other aspects of retirement plans, it is about following a process and making sure all the tools are available to enable participant success.

Grimes and Company has a dedicated team that specializes in providing investment advisory services to retirement plan fiduciaries and their employees. We assist clients with investment selection and monitoring, fee benchmarking, plan design and employee education.

Important Disclosures:

(1) 2023 Retirement Confidence Survey https://www.ebri.org/docs/default-source/rcs/2023-rcs/rcs_23-fs-1_confid.pdf?sfvrsn=738d392f_4

(2) 2023 401(k) Participant Study Charles Schwab https://www.aboutschwab.com/schwab-401k-participant-survey-2023

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company, Inc. [“Grimes”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Grimes is engaged, or continues to be engaged, to provide investment advisory services. Grimes is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Grimes’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at https://www.grimesco.com/form-crs-adv/. Please Note: Grimes does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Grimes’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Grimes client, please contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.