On Saturday, Sept. 20, as I performed my weekend ritual of preparing for the week to come and reviewing market charts, I noticed a number that stuck out to me: The S&P 500 stood at 6664.

I have been an investor and advisor for a long time now, and I have seen a lot. Many on Wall Street have not experienced a recession or a market crisis that lasts longer than a month, but I started my career during the last huge bubble in the late 1990’s as the internet boom reverberated. My contemporaries and I subsequently were forced to navigate the lost decade, complete with two recessions and the nightmarish crescendo of the Global Financial Crisis (GFC). At the very bottom, after the markets got crushed for nearly two years, losing over 50% of value, with the government forced to overtly bail out huge banks and car companies, unemployment spiking to 10%, and money market funds “breaking the buck”, the market bottomed at 666 intraday on March 6, 2009.

Reflecting on the mental wounds left from the first half of my career, I was struck by the simple math that the S&P was now up almost exactly 10X from that scary time: 666 to 6664. What a long, strange trip it has been. (Disclosure – for this piece I am just looking at price action and not considering dividends or the impact on total return.)

Chart 1

Ten times from the abyss, that struck me as simply amazing. There are contributing factors that made this period very unique. Since that time, we had a decade of incredible stimulus from the government, Fed, and Treasury that effectively distorted markets and interest rates across the yield curve. The most amazing feat was the $6 trillion dropped on the economy to make the global pandemic look like a blip on the chart. Another unique aspect is the narrow market leadership with the outsized impact of the biggest technology companies. I am sure that everyone is tired of the analysis that shows how a very narrow group of the largest stocks (Mag 7) account for the lion’s share of all returns and that the average stock is far less. Still, 10X makes a great cocktail party topic. My next thought was, how does this compare to the rest of the world? We all know the answer: Large U.S. companies have left everything else in the dust, but by how much?

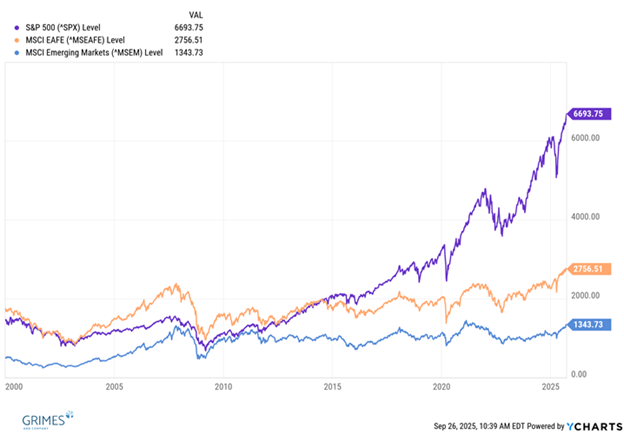

Chart 2

Looking at the MSCI EAFE index (EAFE stands for Europe, Australia, and the far East), that index is up just about 3X from the bottom and only a couple percentage points higher than the highs set before the GFC in 2007. The MSCI Emerging Markets index (China, Latin America, Eastern Europe, among other smaller developing countries) is also 3X from the very bottom and still below the 2007 top (again, all measured on price without impact of dividends). To be fair, the emerging markets were by far the best performing segment to invest in from the turn of the century to that point, but let’s not muddle a great narrative here. During the recovery post-GFC, the U.S. has reigned supreme and American exceptionalism has endured.

The goal of this article is not to be predictive, but simply to just reflect on the incredible journey the markets have been on. I would describe the path that large U.S. stocks have taken as incredibly impressive and amazingly resilient. What will the next chapter bring? Outperformance from one part of the world for this long a duration is probably not sustainable in the long run.

Then again, the long run is hard or even impossible to define. Debt, deficits, valuation, inflation, and over-investment are forces that can lay dormant for long periods of time, but historically they eventually come home to roost, often when least expected. On the other side, innovation and entrepreneurialism have been uniquely American during this period, and the resulting advancements and efficiencies are driving incredible results.

Trees do not grow to the sky, but they grow for a very long time.

Important Disclosures:

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company Wealth Management, LLC (d/b/a Grimes & Company), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Grimes is engaged, or continues to be engaged, to provide investment advisory services. Grimes is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Grimes’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at https://www.grimesco.com/form-crs-adv/. Please Note: Grimes does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Grimes’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Grimes client, please contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian./