The market recovery reflects the economic recovery, via an improvement in S&P 500 profits. According to FactSet’s Earnings Insight report, S&P 500 earnings are forecasted to increase 64% y/y in Q2’21, reflecting the significant improvement over Q2’20 pandemic depressed economy. More significantly, the Q2’21 eps estimate has risen 7% over the past 3 months, versus the 10 year of a 4% decline, and the biggest increase since Factset started tracking this data in Q2’02 (and the prior record was 6.5%, set in Q1’21). While the former point tells us the obvious fact that businesses are going to do much better in Q2’21 than Q2’20, the latter point shows that Q1’21 eps reporting season was historically strong, allowing Q2’21 eps forecasts to rise by so much. While this is good news for the ongoing corporate profit recovery, it also means market expectations are elevated, one of several statistics showing signs of reaching a peak.

A key part of the recovery narrative has been the high level of fiscal stimulus. This, too, has spurred never before seen records. Even though the stimulus packages started in 2020, the programs continued to boost the economy Q1’21 ($900b CARES Act 2, passed on 12/26/20) and Q2’21 ($1.9 trillion American Rescue Plan, passed on 3/11/21). The combination of the large boost in incomes, paired with restrictions on what types of spending could occur, has caused a surge in savings.

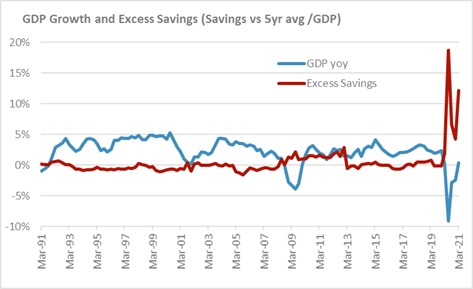

The chart shows year over year GDP growth and Excess Savings. Excess savings is savings (Personal Income – Personal Spending), minus the 5 year average savings rate, divided by total GDP. In Q2’20, this reached 19% of GDP. While it dipped in Q3’20 and Q4’20, it surged back to 12% in Q1’21 from CARES 2 and will also be high in the yet to report Q2’21 data. According to researchers at the Kansas City Federal Reserve, excess savings may have reached $2 trillion. Similarly, if you take the average excess savings from the chart above for Q2’20 through Q2’21, 10.4%, and multiply it by $21 trillion in US GDP, you get a similar $2.1 trillion.

As a reminder: saved money does not get spent and show up in GDP. Instead, it serves as stored spending to be released in future periods. Even though the US is already well on its way to a re-opening recovery, this added stimulus will continue to support economic activity through the end of 2021. While this may seem repetitive, the US economy has never had this level of savings and therefore no one has ever observed how such an economy will perform. The part that is predictable is that demand will remain elevated as consumers return to old habits supported by this pent-up resource setting the table for a strong second half economic recovery.

One example of the surge in demand relative to capacity is the labor market. One of the most notable surprises in the economic data in Q2’21 was a slowdown in payroll growth. Despite the reopening economy, April payrolls increased by only 278,000 (compared to expectations of closer to 1m). But unlike a typical slowdown, when lower economic activity requires fewer workers (i.e. lower demand for workers), in this case the issue was a supply shortage: businesses wanted to hire but could not find enough workers. This has been covered in depth in prior newsletters, but the overall point is excess demand is outstripping supply, and prices (wages) has been rising.

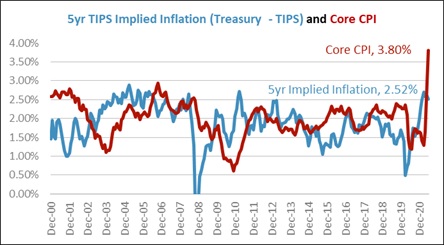

The confluence of restricted supply and surging demand has caused price to rise, more commonly known as inflation. After the word “taper”, the most frequently cited term in Fed coverage has been the word “transitory”. The hope is that inflation is transitory, meaning a temporary issue. There are clearly numerous factors that have caused inflation to jump on a temporary basis. The single most notable is the year over year comparison to Q2’20, which makes even a return to normal inflation seem like a jump. But as economies have reopened, the combination of surging demand and still disrupted supply chains has caused the prices of many products to jump. This has included lumber, houses, and semiconductors. Auto prices have surged as certain supply shortages have caused production shortfalls. May delivered a record headline year over year CPI of 4.9%. Even stripping it down to the Core CPI, it was still +3.8%, as shown in the chart.

But the market agrees with the Fed, and sees the inflation jump as at least partially transitory. This is evident in implied 5yr inflation rate in the TIPS market (based on the 5yr Treasury yield minus the 5yr TIPS yield) at only 2.52%. This indicates that it is likely inflation slows from these record levels as 2021 progresses. There is one catch. With the 10yr Treasury yielding just 1.45% as of 6/30/21, the bond market is not offering good compensation for a world with 2.5% inflation, let alone 3.8%.

Fiscal stimulus has been significant and will boost the economy into the second half, but there will be no more spending programs of that magnitude. Profit expectations are also elevated after a strong Q1 reporting season. Meanwhile, inflation has jumped due to a surge in (hopefully) transitory factors and the labor markets are strained, showing the economic recovery is going about as fast as it can. Due to the major drop in Q2’20 activity, Q2’21’s year over year comparison will inevitably show the highest rates, whether its economic and profit growth or inflation. This has market observers questioning if the economy has reached “peak growth” and if it’s all downhill from here. Markets trade on new, or marginal data. The question is if the rate of positive developments will be Peaking Around the Corner?

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company, Inc. [“Grimes”]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. Please remember to contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing / evaluating / revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Grimes is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Grimes account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Grimes accounts; and, (3) a description of each comparative benchmark/index is available upon request.

The information contained herein is based upon sources believed to be true and accurate. Sources include: Factset Research Systems Inc., Bureau of Economic Analysis, Bureau of Labor Statistics, Congressional Budget Office, Board of Governors of Federal Reserve System, Fred: Federal Reserve Bank of St. Louis Economic Research, U.S. Department of the Treasury

-The Standard & Poor’s 500 is a market capitalization weighted index of 500 widely held domestic stocks often used as a proxy for the U.S. stock market. The Standard & Poor’s 400 is a market capitalization weighted index of 400 mid cap domestic stocks. The Standard & Poor’s 600 is a market capitalization weighted index of 600 small cap domestic stocks.

-The NASDAQ Composite Index measures the performance of all issues listed in the NASDAQ stock market, except for rights, warrants, units, and convertible debentures.

-The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of 21 emerging markets. The MSCI All Country World Index is a free float adjusted market capitalization index designed to measure the performance of large and mid and cap stocks in 23 developed markets and 24 emerging markets. With over 2,800 constituents it represents over 85% of the global equity market.

-The Barlcays Aggregate Index represents the total return performance (price change and income) of the US bond market, including Government, Agency, Mortgage and Corporate debt.

-The BofA Merrill Lynch Investment Grade and High Yield Indices are compiled by Bank of America / Merrill Lynch from the TRACE bond pricing service and intended to represent the total return performance (price change and income) of investment grade and high yield bonds.

-The S&P/LSTA U.S. Leveraged Loan 100 is designed to reflect the largest facilities in the leveraged loan market. It mirrors the market-weighted performance of the largest institutional leveraged loans based upon market weightings, spreads and interest payments.

-The S&P Municipal Bond Index is a broad, comprehensive, market value-weighted index. The S&P Municipal Bond Index constituents undergo a monthly review and rebalancing, in order to ensure that the Index remains current, while avoiding excessive turnover. The Index is rules based, although the Index Committee reserves the right to exercise discretion, when necessary.

-The BofA Merrill Lynch US Emerging Markets External Sovereign Index tracks the performance of US dollar emerging markets sovereign debt publicly issued in the US and eurobond markets.

-The HFRI Fund of Funds index is compiled by the Hedge Funds Research Institute and is intended to represent the total return performance of the entire hedge fund universe.