Is Your Retirement Plan Advisor a Fiduciary?

Are you a fiduciary? If you make decisions that impact your company’s retirement plan, then you are most likely a fiduciary as defined by the Employee Retirement Income Security Act of 1974 (ERISA). It’s also a question you should feel comfortable asking your 401(k) advisor, since many employers look to their investment advisor to help shoulder this responsibility.

In general, an ERISA fiduciary is anyone who exercises discretionary authority over a plan or its assets, or someone who gives investment advice to the plan. A retirement plan advisor that acts as a fiduciary is held to a higher standard of conduct overall and can even share in the fiduciary responsibility that resides with you as an employer.

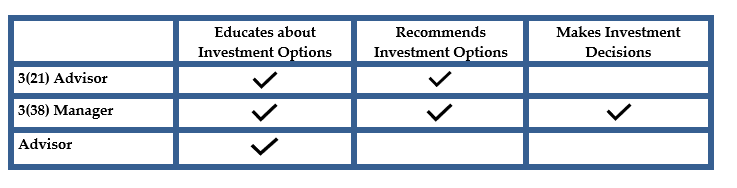

Typically, a retirement plan advisor will act as either a 3(21) Investment Advisor or a 3(38) Investment Manager. In both cases the advisor will offer similar services, including monitoring a plan’s investments, benchmarking fees, and offering employee education. However, there is a distinction between the two titles.

A 3(21) Investment Advisor reviews the plan’s investments and makes recommendations, but they do not have discretion to make the changes. Ultimately, the responsibility to make investment decisions still rests with the plan sponsor.

A 3(38) Investment Manager reviews the plan’s investments and has full discretion to choose and/or replace the investments within the plan. A 3(38) Investment Manager assumes full responsibility for the plan investments and as such, provides a higher degree of fiduciary protection for you as plan sponsor. But remember, the plan sponsor still retains liability in terms of selecting and monitoring the 3(38) Manager.

If you are a decision maker for your company’s 401(k) plan, you should ask this question and make sure you have the right type of plan advisor supporting you.

Grimes has a dedicated team that specializes in providing investment advisory services to retirement plan fiduciaries and their employees. We assist clients with investment selection and monitoring, fee benchmarking, plan design and employee education.

401(k) News: SECURE 2.0 Act Roth Catch-Up DELAYED

The SECURE 2.0 Act was signed into law late last year and made significant changes to many of the rules and regulations governing retirement plans starting in 2023 and 2024. There are over 90 new provisions as a part of the legislation, with the overall goal to encourage more people to participate and save for retirement.

One of the more controversial new provisions originally required workers making $145,000 or more to contribute their catch-up contributions on a Roth basis as opposed to pretax starting January 1, 2024. There was a great deal of confusion as to how to implement this change as it will require new administrative procedures for 401(k) recordkeepers and new coding from employer and payroll companies.

As a result of this, more than 200 entities, including the American Retirement Association, petitioned the U.S. House Ways and Means to delay the Roth catch-up rule for two years, until 2026. As a result, the IRS issued Notice 2023-62, which granted a two year transition period through December 31, 2025 to allow for compliance with this specific provision. So, we now have until 2026 to figure out how to account for this new rule.

Important Disclosures:

Sources include eSignal.com, Bureau of Economic Analysis, Bureau of Labor Statistics and FactSet.

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company, Inc. [“Grimes”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Grimes is engaged, or continues to be engaged, to provide investment advisory services. Grimes is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Grimes’ current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at https://www.grimesco.com/form-crs-adv/. Please Note: Grimes does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Grimes’ web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Grimes client, please contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.